Calls to combat climate change are reaching deafening levels across the international community. Study after study shows the links between anthropogenic greenhouse gas emissions and the devastating effects on our planet’s changing climate. Catastrophic species loss, fundamental changes in ecosystems across the globe, and food and water scarcity forcing millions into poverty are only a few effects of unchecked climate change. Among developed and developing nations alike, electricity generation creates a substantial amount of greenhouse gas emissions. This fact has led to a global energy transition away from traditional fossil fuels to renewable energy sources. However, current and planned policies will fail to limit warming below 2℃. With immediate, aggressive action needed across the international community, this Article explores energy policy frameworks within the European Union (“EU”) and United States (“U.S.”) that seek to address climate change by fostering renewable energy source growth. I believe that the EU and U.S. require increasing regional and subnational cooperation to reach and improve upon their policy goals. The EU has linked its broad decarbonization efforts and energy transition to successfully completing the EU Internal Energy Market. As a result, the EU must now complete critical interconnection projects to enable the internal energy market, or its transition to renewable energy sources may stall. Should interconnection goals fail to materialize, member states will likely shift to low-cost natural gas as renewable energy becomes congested and blocked at key points throughout the EU. Further, the tremendous increase in natural gas production and its continuing low cost have fundamentally altered the EU and U.S. energy landscapes. Key policy tools in the U.S., like renewable portfolio standards, require adjustment as market forces, driven by the low cost of natural gas, may inhibit future renewable generation capacity. These results suggest that both the EU and U.S. energy futures will be dominated by natural gas, wind, and solar energy, as coal can no longer be cost competitive. Therefore, in the global discourse on energy transitions and reducing energy related greenhouse gas emissions, the discussion must turn to focus on regional cooperation and avoiding increasing reliance on natural gas.

I. The International Effects of Climate Change and the Global State of Climate Action

Climate change is the defining issue of our time. The effects of our warming planet and their link to human activities now dominate international discourse as governments and their citizens demand action. In response, climate action seeks to reduce greenhouse gas (“GHG”) emissions. Climate change’s severity in the coming decades will depend on how countries around the world reduce their GHG emissions. Reports from the Intergovernmental Panel on Climate Change (“IPCC”),[2] United Nations Environment Programme (“UNEP”),[3] United States Global Change Research Program,[4] and International Energy Agency[5] all show that drastic reductions in GHG emissions must occur to limit the effects of climate change. Of the various human activities that produce GHGs, energy production and use are the largest GHG emissions sources globally.[6]

In 2017, energy related CO2 emissions accounted for over half of global GHG emissions.[7] As a result, governments rightfully looked to their energy sectors for the most impactful reductions in GHG emissions. Therefore, this Article will discuss: (1) where nations can achieve the greatest gains in energy related emissions reductions, and (2) how certain nations are approaching and realizing these reductions, learning from their challenges, and determining solutions. Doing so will endow readers with an international perspective on climate change policy, effects, and the ability to identify key areas for improvement going forward. Placing energy related emissions in the context of larger climate action will give global GHG emissions and climate change policy broader goals. Additionally, this Article will present the effects of failing to reduce GHG emissions, conveying the urgency and immediate need for climate action. After presenting global emission levels, the primary source of emissions, and future targets for reduction, this Article will compare European Union (“EU”) and United States (“U.S.”) policy approaches to promote renewable energy sources (“RES”). Both the EU and the U.S. are leading GHG emitters but approach climate change from differing, and at times opposing, viewpoints. Comparing their similarities, differences, and likely effectiveness allows identification of key areas for improvement and implementation of strategies to combat climate change and effectuate a transition to RES.

International climate change action seeks to reach net-zero global anthropogenic CO2 emissions that will, in turn, limit expected increases in global temperatures. The IPCC study on 1.5℃ warming and climate change effects concluded that anthropogenic emissions “up to the present are unlikely to cause further warming of more than 0.5℃ over the next two to three decades or on a century timescale.”[8] However, under current policies, increasing global GHG emissions show no sign of slowing, and projected emissions are expected to result in temperatures increasing over 3℃ by 2100 and continuing thereafter.[9] To understand and compare how these increases in temperature will affect both people and the environment, the international scientific community has focused its studies on the effects from global temperature increases between 1.5℃ and 2.0℃.

Comparing the expected effects from warming between 1.5℃ and 2.0℃ reveals how global temperature increases affect both people and the environment. Further, the comparison highlights the effect even a 0.5℃ increase causes and the critical need to limit such increase. Warming between 1.5℃ and 2.0℃ will increase the frequency, intensity, and duration of heat-related events.[10] In turn, the frequency and intensity of droughts are expected to increase in certain regions while the frequency and intensity of extreme rainfall events are expected to increase in others.[11] These effects shift climate zones poleward, which increases drought, wildfires, and pest outbreaks in high-latitude regions and causes climatic conditions in tropical regions that have not occurred during the twentieth century—conditions characterized by high temperatures with strong seasonality and shifts in precipitation.[12] These climatic changes threaten food supply stability as food chains are disrupted and the nutritional quality of crops decreases.[13] Warming will also likely result in increased desertification that reduces biodiversity, increases water stress, and amplifies environmentally induced migration around the world.[14] These migrations will be further spurred by rising sea levels that are projected to continue rising even beyond the next century.[15]

Higher temperatures amplify the effects of our warming planet. Studies from the IPCC show marked increases in the negative effects from climate change between 1.5℃ and 2.0℃.[16] The IPCC finds a 0.5℃ increase in global temperature from 1.5℃ to 2.0℃ likely results in increased sea-level rise.[17] The increase would expose over ten million more people to risks from saltwater intrusion, flooding, and infrastructure damage.[18] The increased rate of sea level rise under a 2.0℃ scenario will also greatly limit communities’ ability and opportunities to adapt to and manage those risks.[19] Ecologically, the IPCC studied over 100,000 species and concluded that under a 1.5℃ temperature increase scenario, six percent of insects, eight percent of plants, and four percent of vertebrates would lose over half of their geographic range.[20] Under a 2.0℃ increase scenario, those percentages at least doubled.[21] The doubling effects between a 1.5℃ to 2.0℃ increase were similarly found in the percentage of terrestrial land expected to transform from one ecosystem type to another and the expected decrease in yields from fisheries.[22] Critically, climate change will disproportionately affect developing and disadvantaged populations. These communities include those dependent on agricultural and coastal livelihoods and developing nations that will struggle to adapt. The IPCC estimates that limiting warming to 1.5℃ compared to 2.0℃ “could reduce the number of people both exposed to climate-related risks and susceptible to poverty by up to several hundred million by 2050.”[23] Devastatingly, current policies make limiting warming to 1.5℃ an impossibility.

B. The Emissions Gap and Inadequate National Policies

The emissions gap represents the difference between global GHG emissions under current Nationally Determined Contributions (“NDCs”) and total global emissions in 2030 required to keep the planet on the least-cost path to limiting warming between 1.5℃ and 2.0℃.[24] NDCs are voluntary pledges made by nations under the Paris Agreement to reduce emissions and combat climate change.[25] UNEP estimates that even if nations meet current NDCs, the emissions gap to limit warming to 2.0 ℃ will be around fifteen GtCO2 and thirty GtCO2 to limit warming to 1.5℃.[26] For perspective, UNEP calculated global GHG emissions in 2017 were around forty-nine GtCO2.[27] To limit warming to only 2.0℃, UNEP concluded that global emissions should be around forty GtCO2 in 2030.[28] If nations achieve only current NDCs, UNEP and the scientific community project a mean global temperature increase around 3.0℃.

However, nations cannot guarantee they will be able to meet their current NDCs. As commentators repeatedly point out, the Paris Agreement contains no specific target, date, means for coordinating contributions among nations, or enforcement mechanism. If a nation fails to meet a target, doesn’t set an ambitious enough target, or wishes to abandon the Agreement, they face no meaningful consequence.[29] Rather, the Paris Agreement relies on nations presenting progressively more enhanced reduction contributions every five years, simply based on good will.[30] Taken together, the emissions gap and NDCs under the Paris Agreement highlight the reality that limiting warming to 2.0℃ or below will require individual nations to commit to far more aggressive GHG reductions.

The largest GHG emitters must realize far more aggressive policies to limit warming to 2.0℃ or below. Currently, the largest GHG emitters are China (26.8%), the U.S. (13.1%), the EU (9%), and India (7%).[31] Under current policies and NDCs, all four nations are expected to remain the largest emitters with India overtaking the EU and rivaling the U.S. by 2030.[32] Based on their expected 2030 emissions, to close the emissions gap for 2.0℃ solely from reductions by the largest four emitters, each nation would have to reduce their projected emissions by around forty percent.[33] With current policies not achieving the required reductions to limit warming to 2.0℃ or below, nations will have to find ways to make further reductions.

II. Reducing Energy Related Emissions to Close the Emissions Gap

Together, the U.S. and the EU produce almost a quarter of global GHG emissions.[34] However, the U.S. and the EU have had wildly different histories with climate change policy. Since international climate action began with the United Nations Framework Convention on Climate Change, the EU has pushed for binding emissions targets and timetables.[35] The U.S., under every administration, has either been unable to incorporate binding climate policy or outright rejected it.[36] Where the U.S.’s inability to incorporate international reduction targets or otherwise effectuate such international policy has become an accepted feature in international climate policy, both the EU and certain U.S. states are actively pursuing reductions in GHG emissions.

Barring the lack of binding law, both the EU and U.S. states are increasingly focused on reducing energy related emissions. In 2017, energy related emissions accounted for over half of global GHG emissions.[37] For the EU and U.S., fuel combustion and fugitive emissions from fuels, excluding transportation sources like cars and trucks, accounted for the largest amount of each country’s emissions.[38] Within energy related emissions, countries focus on reducing their reliance on coal to produce energy. In 2017, the International Energy Agency estimated that coal generation accounted for 9.84 GtCO2—almost a third of energy related emissions.[39] In the U.S., around two-thirds of electricity generation emissions come from burning coal.[40] Replacing coal fired generation around the world with renewables will translate to the greatest, most immediate reduction in energy related emissions, and thereby global emissions.

III. Europe’s Commitment to Renewable Energy

Since the formation of the United Nations Framework Convention on Climate Change in 1992, the EU has approached climate change action from the top-down through binding emissions reduction targets. The EU’s top-down regulatory approach to climate change has in turn shaped their energy policy and transition from coal to RES. This transition began to take shape in 2009 with the Renewable Energy Directive and has since served as the foundation for EU energy policy.

A. The 2009 Energy Renewable Directive

The European Community enshrined its commitment to RES generation in 2009 with its Declaration on the Promotion of the Use of Energy from Renewable Sources (“RED”). The RED set mandatory targets for EU members that equated to “at least a 20% share of energy from renewable sources in the Community’s gross final consumption of energy in 2020.”[41] These mandatory targets for EU members ranged from a high of forty-nine percent in Sweden to a low of ten percent in Malta.[42] To monitor progress and compliance, the RED created an indicative trajectory for each EU member and required them to submit reports every two years detailing progress toward meeting their target.[43] Should an EU member ever fail to meet their indicative trajectory, the member would have to submit an amended action plan to the European Commission (the “Commission”) for recommendation.[44] As binding EU law, if an EU member failed to meet its target or abide by the directive, infringement proceedings could be brought against them.[45]

B. Revised Renewable Energy Directive

The European Community met and created a revised RED, which came into force on December 11, 2018.[46] The revised RED importantly maintained the mandatory binding targets for renewable energy as set out in the 2009 RED. It also created flexibility and new options for members who may not meet their 2020 targets.[47] Additionally, the revised RED created a new binding target of thirty-two percent for the share of energy from renewable sources in the Union’s gross final consumption of energy by 2030.[48] Where the 2009 RED listed the binding target for each member that would equate to the binding twenty percent target, the revised RED charged members with proposing their own targets.[49] Members were required to submit to the Commission by December 31, 2019 an “integrated national energy and climate plan” (“NECP”) covering the years 2021 through 2030 and containing, among other requirements, their proposed targets for 2030.[50] Arguably an expanded version of the older National Action Plans, the NECPs would then be analyzed by the European Commission to determine whether the integrated plans would collectively meet the thirty-two percent target.

The revised RED greatly expands the Commission’s power compared to the original 2009 RED. The Commission now has authority to review member-proposed NECPs and broad powers to issue recommendations related to both proposed member plans and “any additional policies and measures that might be required” in the plan.[51] Members must specifically address those recommendations in their revised NECPs or provide reasons why they have not.[52] While unable to draft an EU member’s NECP, it appears the Commission could effectively rewrite a member’s NECP later on. Under the revised RED, if the Commission finds a member’s NECP is “insufficient for the collective achievement of the Energy Union’s objectives,” the Commission can “propose measures and exercise its powers at Union level in order to ensure the collective achievement of those objectives.”[53] As EU members contemplate this new power and push toward meeting and maintaining their 2020 binding targets for renewable energy, the revised RED also sets a fifteen percent binding interconnection target for members to reach by 2030—linking the EU movement to decarbonize with the goal of creating an EU “Internal Energy Market.”[54]

C. The EU Internal Energy Market and Its Linkages to the RED

Establishing an EU Internal Energy Market (“IEM”) can be broadly conceptualized as no EU member being isolated from European electricity and gas networks.[55] The Commission views completing the IEM as a prerequisite for supplying affordable, sustainable electricity for all.[56] Delivering on this lofty goal requires numerous infrastructure, market, and policy advancements tied together by unprecedented cooperation and coordination between EU members. Understanding the key advancements that the Commission felt were necessary in 2014, and analyzing their progress towards completion, reveals important realities surrounding the IEM’s current state. Further, through the analysis, linkages can be seen between the EU’s ability to create the IEM and meeting the revised RED’s goals.

The Commission takes an EU-wide view of electricity and gas production. The Commission believes that EU members pursuing self-sufficiency in electricity and gas production is “no longer sensible or efficient.”[57] With this view, the Commission identified two key goals to reach by 2020. First, to reach an average ten percent interconnection among EU members.[58] Second, to complete seventy-five percent of the EU’s list of 248 Projects of Common Interest (“PCI”).[59] The Commission believed that completing PCIs was urgently needed to strengthen the IEM and that their designation as PCIs would allow the projects to benefit from “more efficient permit granting procedures.”[60] Neither goals were completed before the end of 2020.

Both the ten percent average interconnection among EU members and seventy-five percent completion of the PCIs were not realized by 2020. The Commission acknowledges that while some EU members will reach the ten percent interconnection target, others will not.[61] PCI completion has been abysmal—even after the Commission reduced the total PCIs to be completed since 2014. Of the 110 electricity PCIs on the list in 2017, only one percent had been commissioned.[62] Further, even based on self-reporting, only twenty-five percent of PCIs were expected to be complete by 2020 with seventy-five percent expected sometime in 2024.[63] Gas fared far worse with none of the fifty-three gas PCIs commissioned as of 2017.[64] Again, based on self-reporting, only sixty-four percent of gas PCIs are expected to be commissioned by 2022—a reality the Commission admits is “highly uncertain.”[65] The Commission’s findings about what has caused such categorical failures in PCI completion and interconnection targets reveal important implications for the revised RED’s and the IEM’s futures.

ii. Infrastructure Implications and Linkages

The Commission’s findings show that immense permitting delays among EU members have led to a bottleneck in PCI completion. Further, due to new energy realities, the formula originally created to measure interconnectivity is flawed and tends to lead to decreasing interconnectivity measurements. For over half the electricity PCIs, the Commission found a ten-year average expected commission timeframe after planning begins.[66] The most frequent reasons given for delays in permit granting were environmental concerns or national law changes.[67] The Commission claims that PCIs have a more efficient permit granting process, so PCI’s constantly citing permitting delays as the reason for not meeting timelines should cause great concern at the national level.

The Commission found that a reason for EU members failing to meet the interconnection target is the formula used to measure interconnection. Under the original formula, the Commission found that the increase in generation capacity among EU members from RES coupled with a slower increase in interconnection capacity leads to linear decreasing of an individual member’s interconnection level.[68] The original formulation for interconnectivity was created when only “2% of total energy was generated from variable, non-dispatchable sources and where the discrepancy between installed generation capacity and the peak load was negligible across Europe.”[69] While this formula would offer continuity, the Commission recommended that the current formula be changed to account for interconnector benefits and prerequisites post-2020.[70] This finding suggests that EU members should reconsider the target formulation within the revised RED to ensure they adequately account for the effects from increased renewable energy capacity.

iii. Policy Challenges, Implications, and Linkages

The Commission identified taking a regional approach in developing the IEM as a key requirement for its success.[71] The Commission also identified the need to correct uncoordinated and counterproductive national measures that damage a successful IEM.[72] EU members were directed to ensure that policy interventions in their markets to promote renewable energy sources were necessary, proportionate, and designed to facilitate market integration.[73] Looking back, harmony in policy, reduced state interventions, and network codes that enable a successful IEM have been achieved with only mixed success.

Harmony in policy and reduced state interventions tend to be directly related—increased harmony and coordination between EU members should limit state interventions. Since 2014, however, a dramatic rise in state intervention has occurred.[74] The Commission found that the commitment to decarbonize and the later increase in generation from RES has had practical and political consequences leading to such interventions.[75] The Commission also found that current market rules are not conducive to RES’s variable nature.[76] Further, as EU members sought to meet their own 2020 renewable energy targets, they did so at a national level, resulting in “sub-optimal rules for the support of RES generation.”[77] These uncoordinated support schemes led members to introduce measures, known as capacity mechanisms, to both protect existing and create new generation. These national interventions necessarily had significant effects on the markets; the Commission found that the interventions ultimately “neutralis[ed] the positive developments on wholesale electricity markets and d[rove] up prices for end customers at the retail level.”[78] Increased RES generation has also pushed network operators to engage in practices that inhibit a successful IEM.

Increased RES generation has created other challenges for transmission system operators (“TSOs”)—especially in effective interconnector utilization. The Commission identified uncoordinated interconnector use as a “key barrier to cross-border trade.”[79] The Commission found that where interconnection capacity exists between countries, TSOs are preventing up to seventy-five percent of the physical interconnection capacity from being available to the market.[80] The reason for this behavior among TSOs was found to be their increasing need to avoid stability problems within their own grids.[81] The Commission found that one main reason for TSOs limiting capacity in this manner was the “increase of volatile generation from wind and sun,” and TSOs’ internal grids being unable to accommodate the production.[82] The Commission’s findings show that not only have the issues identified in 2014 not been tackled, they have also gotten significantly worse. The reality emerges that where the EU has created broad frameworks to increase RES production, it has stumbled in achieving its goals. This has happened because the EU took isolated national action instead of implementing the regional approaches embodied in both the IEM and revised RED. Where the EU has pursued a broad, top-down approach to its climate and energy policy, the U.S. has taken a drastically different approach.

IV. The United States’ Fragmented Approach to Combatting Climate Change

Compared to the EU’s methodical, top-down approach to climate policy, climate-related action in the U.S. can best be categorized as a fragmented, bottom-up approach. The U.S. must take aggressive action to help meet its 2030 emissions targets, but meaningful climate-related policy action occurring at the national level is unlikely. Facing this reality, U.S. climate policy has thus far been concentrated at the state level.

In the vacuum left by the absence of national climate policy, some states have stepped up to fill the void with varying degrees of success and ambition. This state action has been described as defying economic logic under traditional economic theory.[83] Indeed, states as individual small emitters are thought to have little incentive to curb their emissions without other states agreeing to similar emissions reductions.[84] However, after the Trump administration pulled out of the Paris Agreement, twelve states immediately informed the federal government that they believed the U.S. should remain in the agreement.[85] Today, twenty-four states, Puerto Rico, and the District of Columbia have joined the United States Climate Alliance (“Climate Alliance”).[86] Their goal is to “implement policies that advance the goals of the Paris Agreement, aiming to reduce greenhouse gas emissions by at least 26-28 percent below 2005 levels by 2025.”[87] With over five GtCO2 in energy related emissions in 2016, coordinated state action has the potential to drastically affect total U.S. GHG emissions.[88]

A. Current State Policy and Energy Emissions

U.S. state action has the potential to make significant GHG emissions reductions over the coming years. A decade ago, few state programs promised significant GHG reductions, and greater state cooperation was identified as the key to future climate policy success.[89] According to the U.S. Energy Information Administration (“EIA”), the current twenty-four states that comprise the Climate Alliance account for almost forty-two percent of U.S. energy related emissions.[90] If these States meet their emissions targets, they will reduce total yearly U.S. energy related emissions by almost 260 MtCO2, or four percent of total 2017 U.S. emissions.[91] If all fifty states reached similar targets, yearly U.S. energy related emissions would be reduced by 800 MtCO2, or almost 12.5 percent of total 2017 U.S. emissions.[92] Even if all fifty states met the original U.S. pledge in reductions under the Paris Agreement, the fifteen GtCO2 and thirty GtCO2 emissions gap to limit warming to 2.0℃ and 1.5℃ respectively would remain.[93] Therefore, to determine what steps the U.S. can take to make further reductions, it is critical to understand what the states are currently doing to reduce emissions.

B. The Interplay Between State Policy and Power Markets

States have tremendously influenced RES growth through Renewable Portfolio Standards. In doing so, states have fostered markets where RES now compete with traditional fuel sources like coal, nuclear, and natural gas.[94] Understanding U.S. electricity markets at a high level, and the interplay between fuel sources and policy, presents a means for shaping and creating effective future policy. In 2018, total U.S. electricity generation was over four trillion kW/h.[95] The 2018 U.S. generation mix was comprised of approximately thirty-eight percent natural gas, twenty-three percent coal, twenty percent nuclear, and seventeen percent renewables.[96] For the past decade, almost all power plant retirements have been fossil fuel powered, predominately coal, while almost half of all capacity additions have come from RES.[97] This trend is expected to continue in the coming years.[98] The current and projected fuel mix, along with retirements, show that the U.S. energy future will be one powered predominately by natural gas and renewables, as coal recedes from the generation mix. Therefore, in shaping and encouraging RES growth, these trends reveal that natural gas plays a critical role in influencing RES additions.

C. State Policies to Reduce Energy Related Emissions

States have historically used Renewable Portfolio Standards as the primary method to reduce energy related emissions and transition to RES. Renewable Portfolio Standards require a certain percentage of electricity that a utility company sells to be generated by RES.[99] For example, California’s Renewable Portfolio Standards currently requires sixty percent renewable energy by 2030 and 100 percent renewable energy by 2045.[100] Since 2000, Renewable Portfolio Standards have accounted for around half the total RES growth in the U.S.[101] While Renewable Portfolio Standards have spurred RES growth, no two state’s standards are the same. The standards vary widely in their importance in driving an individual state’s RES growth along with other key factors such as targets, timeframes, and enforcement.[102] For example, Renewable Portfolio Standards were central to RES growth in the Northeast, Mid-Atlantic, and Western portions of the U.S.; however, they have only minorly influenced new RES capacity in Texas, the Midwest, and Southeast portions of the country.[103] Importantly, in regions where Renewable Portfolio Standards have been key drivers of RES growth, such as California, policy trends show increasingly more ambitious targets.[104]

In addition to setting Renewable Portfolio Standards, states must enforce those standards to ensure achievement. In their 2018 compliance reports, most states and utilities met or exceeded their interim targets.[105] However, some states are only meeting their interim targets by relying on stockpiled Renewable Energy Credits (“credits”).[106] Using stockpiled credits is troubling because it means those states are meeting their targets through a purely financial product and not by adding new RES capacity. Even with some states currently relying on banked credits, projections suggest that RES generation will outpace Renewables Portfolio Standard requirements through 2050.[107] With projected RES generation expected to outpace current Renewables Portfolio Standard requirements, other drivers are necessarily promoting RES growth and state policy.

V. Using LACE-LCOE to Compare Natural Gas, Conventional, and RES Generation

The explosion in U.S. natural gas production has forever changed the country’s energy mix. The surge in U.S. production came from technological advances in natural gas production. These advances have in turn led to strikingly low natural gas prices that have increased investment in new natural gas plants and existing plant use. Low prices of natural gas, lower variable non-fuel operating expenses, and higher efficiency from combined-cycle natural gas plants have driven down wholesale electricity prices in U.S. markets. The lower wholesale electricity prices have put immense pressure on coal and nuclear economic viability. Natural gas competitiveness in the U.S. can be seen from a comparison between the levelized cost of electricity (“LCOE”) and levelized avoided cost of electricity (“LACE”).

Together, LCOE and LACE are effective at measuring different electric generating technology competitiveness. LCOE represents the “installed capital costs and ongoing operating costs of a power plant, converted to a level stream of payments over the plant’s assumed financial lifetime.”[108] Put another way, LCOE represents a technology’s total generation cost that has been broken down into the per unit of electricity cost required to recover plant building and operating costs over its lifetime. While it may be tempting to compare generating source competitiveness based solely on LCOE, this measure alone does not capture other critical factors that go into the decision to choose a given generating technology.[109] Regional differences in project characteristics, generator availability, existing generating mix in a region, and a resource’s capacity value are all critical factors that influence a build decision.[110] For these reasons, the National Renewable Energy Laboratory notes that LCOE alone “should not be used to compare distributed and utility-scale generation technologies.”[111]

LACE seeks to capture the value a power plant adds to the grid. The EIA defines LACE as “a measure of what it would cost to generate the electricity that would be displaced by a new generation project . . . summed over a project’s financial life and converted to a level annualized value that is divided by average annual output of the project.”[112] LACE seeks to capture regional variability by accounting for daily and seasonal variation in electricity demand across a given region. LACE then compares the potential new generation source against the current and new generation mix it will displace.[113] Like LCOE, LACE does not capture all of the key factors that go into a build decision. However, both the EIA and the National Renewable Energy Laboratory, with some qualifications, note that using a LACE to LCOE value-cost ratio gives a greater representation for new capacity addition build decisions.[114]

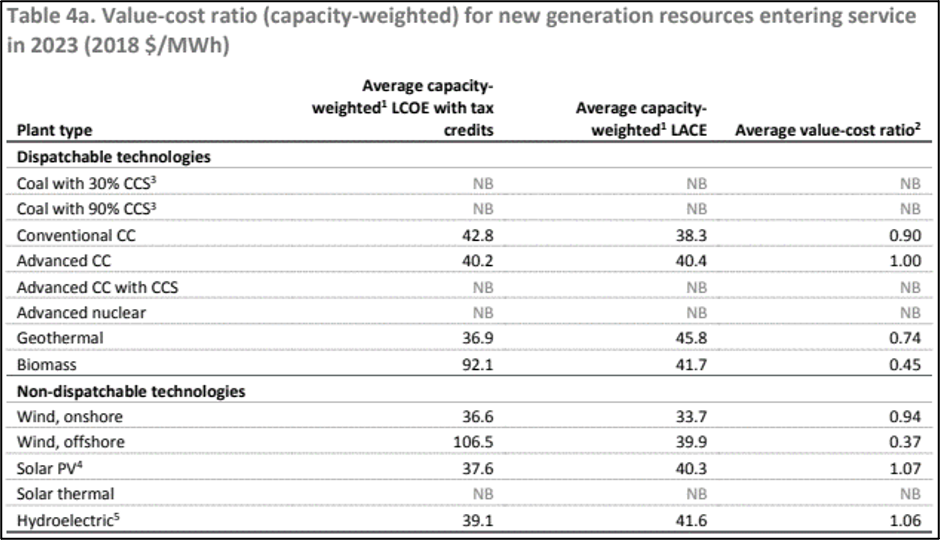

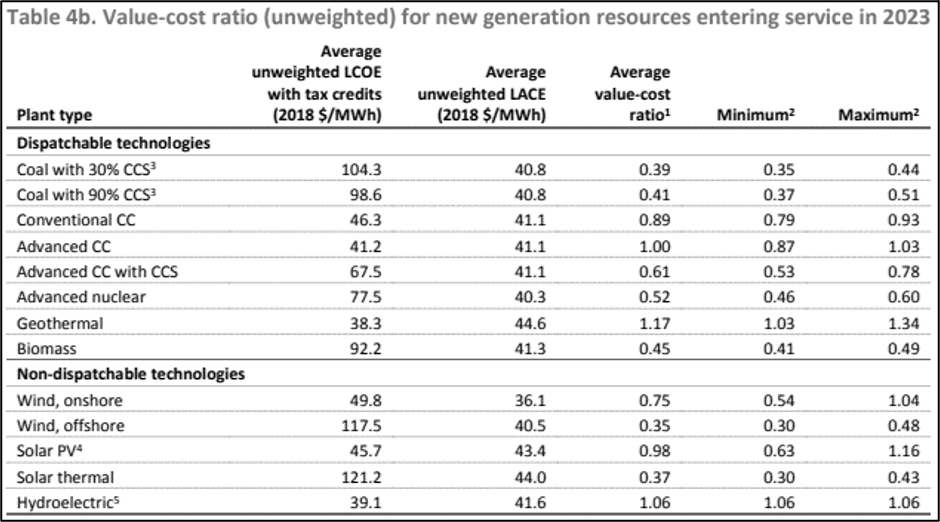

Comparing the value-cost ratio for different generation technologies reveals current trends and future projections for capacity additions. Though LACE to LCOE comparisons do not capture all of the factors that go into a build decision, LACE to LCOE value-cost ratios provide one of the best means to compare a generating technology’s economic competitiveness. When analyzing a technology’s value-cost ratio, a number greater than one means the technology’s value exceeds its cost by displacing costlier generation and capacity options.[115] Where a technology’s value-cost ratio falls below one, the technology’s cost exceeds its value to the system it would belong to.[116] EIA’s LACE and LCOE calculations present two revealing value-cost tables that suggest why the U.S. energy future will likely be dominated by natural gas, wind, and solar generation.

The EIA prepared capacity-weighted and unweighted value-cost ratios for generating technologies entering service in 2023 that signal a move away from new nuclear and coal capacity additions.[117] The capacity-weighted table, in the appendix, shows value-cost ratios weighted by new capacity coming online across the various regions in the U.S. between 2021 and 2023.[118]

The unweighted table reveals that only advanced-combined-cycle natural gas, hydroelectric, and geothermal generation have average value-cost ratios at or greater than one.[119] Solar PV’s value-cost ratio is 0.98, followed by conventional combined cycle at 0.89, and onshore wind at 0.75.[120] Tellingly, both nuclear and coal’s average value-cost ratios fall at half or below-half the value-cost ratio for advanced-combined-cycle natural gas generation and solar PV.[121] Even though the average value-cost ratio does not capture all of the factors that ultimately go into a build decision, the EIA’s study suggests that coal and nuclear are not economically competitive in the future generation mix.

EIA’s capacity-weighted value-cost ratios reveal that advanced and conventional-combined-cycle natural gas, onshore wind, and solar PV represent the most economically competitive generation technologies going forward. The capacity related value-cost ratios are weighted by each source’s new capacity coming online in the U.S. between 2021 and 2023.[122] Weighted in this manner, combined-cycle natural gas, onshore wind, and solar PV all have ratios at, above, or nearly at one.[123] The values reflect that no new capacity additions for coal or nuclear are expected to occur in this time frame. Further, the trend can already be seen in the lack of new nuclear and coal capacity in planned 2020 capacity additions, while wind, solar PV, and natural gas account for ninety-eight percent of new capacity additions.[124] Both present day capacity additions and projections signal that the U.S. energy landscape is moving away from coal and nuclear to natural gas, solar, and wind.

VI. Comparing EU and U.S. RES Policy Frameworks

After understanding the broad policy and economic forces shaping the U.S. energy future, it is possible to compare the EU and U.S. energy realities. While these energy landscapes do not allow a direct policy comparison, comparing the challenges the U.S. and the EU face reveals valuable lessons to improve future policy decisions. The EU has created a robust national policy framework to tackle climate change and enable its energy transition to RES. However, closely examining the revised RED and NECP processes reveals that the EU must overcome crucial stumbling blocks to fulfill its policy ambitions. A key hurdle the EU must overcome is to effectively use the NECP process to its full potential by submitting well-reasoned, specific policy goals and the approaches necessary to achieve the goals. Additionally, by taking an EU-wide approach to its energy transition, member states have critically tied their energy transition’s success to a substantial increase in interconnection capacity between member states. Looking closely at both the NECP process and the need for greater interconnection capacity reveals that the EU now faces a regional and subnational cooperation crisis. Success in fostering such cooperation will in-turn determine success in achieving an inspiring national framework to tackle climate change and promote RES.

Where the EU has succeeded in developing a national framework to tackle climate change and transition to RES, the U.S. has engaged in a fragmented, subnational approach to achieving its climate and energy goals. This historically fragmented approach now offers tremendous opportunity for states to both drastically increase subnational cooperation and develop a foundation for a future national policy framework directed at addressing climate change and the transition to RES. The NECP process provides valuable lessons and considerations for states as they pursue greater cooperation. Applied to current state cooperative efforts, like the United States Climate Alliance, the NECP process could inform the creation of an effective subnational framework. The comparison between the EU and U.S. reveals that both must foster substantial subnational cooperation to achieve their climate and energy goals. The EU must do so to carry out its defined national goals while the U.S. states have an unprecedented opportunity to create a national policy framework.

A. Maximizing National Policy Potentials in the NECP Process

With the revised RED, the EU has created a robust national policy framework to encourage RES growth among its member states. The revised RED also provides other policy advantages that highlight the opportunities a national energy policy framework provides to its members states. By creating a national energy policy framework through the revised RED, the EU has created a platform for member states to identify strengths and weaknesses in each other’s NECPs, areas for improvement, and opportunities for collaboration and investment. A European Commission communication reflecting on submitted draft NECPs and the larger revised RED framework reveals what member states can do to benefit most from the NECP process.[125]

The European Commission identified several ways the NECP process can provide additional benefits to member states. The Commission identified that NECPs can be used to promote the assessment of policy effects among member states, identify and secure necessary energy investments, promote a fair energy transition among member states, and identify opportunities in related policy fields such as the environment.[126] The NECP process provides a structured framework for member states to compare and improve their strategies for RES growth. The Commission suggests member states use the NECP process to assess the interaction between policies and more fully understand their effects.[127] Because correcting uncoordinated and counter-productive national measures are key issues EU members must tackle to create a successful Internal Energy Market, member states must ensure their assessments analyze and account for policy effects on other member states.

The NECP process also allows member states to identify the critical investments needed to meet their energy and climate targets. The Commission points out that an additional 260 billion Euros in investment is needed each year in energy related sectors to deliver on the EU’s 2030 climate and energy targets.[128] So far, member states have estimated their investment needs with varying specificity on how they will source those investments.[129] Member states have a profound opportunity to undertake studies to determine their investment needs, sources, and then share those findings with the larger EU community through the NECP process. Doing so will improve both intra- and inter-member synergies in energy climate policy.

NECPs allow member states to integrate social concerns into their plans. The Commission views the NECP process as a means to form a foundation for a comprehensive policy mix that ensures a just energy transition.[130] Key to promoting a just energy transition will be member states addressing and reducing energy poverty within their own borders.[131] The Commission points out that nearly fifty million people across the EU live in energy poverty.[132] NECPs from Greece, Italy, Malta, and Finland set specific energy poverty objectives and provide good detail in addressing them.[133] The NECP process provides numerous opportunities for member states to effectively address the interconnectedness between energy, climate, and social policies.

The NECP process enables member states to collaborate on societal policies that are bound together with energy and climate. In addition to the EU energy transition’s societal dimension, the NECP process provides opportunities to evaluate environmental effects and opportunities that are intertwined with decarbonization. Member states should be linking their biodiversity, air, and bio-economy policies together with their energy policies to ensure consistency and maximize the “circular economy for decarbonization . . . .”[134] Harmony between energy, climate, social, and environmental policies not only provides new opportunities and benefits within member states, but also for the EU community at large. In addition to holding itself out to assist member states, the Commission identifies several forums where member states can engage in dialogue and share best practices in achieving policy synergy.[135] In sum, the NECP policy framework derives its strength from an interactive approach that champions growth and harmony between member states as they seek to reach their future policy goals.

B. How the NECP Process Can Inform Subnational Action in the U.S.

A national U.S. policy framework to combat climate change and promote RES growth will likely not happen in the short-term. However, the NECP process can inform that framework’s eventual creation by shaping current state action. Assessing policy effects among states, identifying and securing necessary energy investments, promoting a fair energy transition among states, and identifying opportunities in related policy fields present challenges and tremendous opportunities for all states. As states seek to address these challenges, the NECP process provides valuable lessons and highlights the importance of unified action.

The Climate Alliance presents an incredible opportunity for states to form a collaborative foundation to address climate change and promote RES growth. State action to address climate change has been fragmented, with Climate Alliance members agreeing to uphold the goals in the Paris Agreement and then setting off on their own to achieve them. The Climate Alliance provides a summary snapshot for each member state’s goals and policies, publishes an annual report, gives a broad strategy approach for each year, and has published some working group papers.[136] Through the Climate Alliance, states could achieve far greater harmony in policy, develop an iterative approach to combatting climate change, and promote RES growth. States could begin to unify their approach to these issues that have plagued the U.S. for decades. The NECP can inform this process in several ways.

Through the Climate Alliance, member states should develop an interactive policy approach to combat climate change and promote RES growth. The NECP relies on member states to propose RES targets and provide policy goals while the Commission reviews member state proposals and suggests changes.[137] In this way, the Commission can promote policy unity among member states and drive the change member states seek to create. In the same way, the Climate Alliance should begin to set up a similar framework for collaboration. Climate Alliance states should come together to form a representative body that analyzes current and proposed state policy and create a system to spur additional, cohesive policy initiatives across member states. This will be especially important as U.S. states face similar challenges across the spectrum of policy interaction, cohesion, investment, social issues, and related fields such as environmental policy. Today, states are confronting these issues largely alone with mixed success and specificity.[138] The NECP process suggests numerous benefits if Climate Alliance states create their own energy and climate plans, bring them to a multistate forum, and begin the interactive process of analyzing their policies and identifying opportunities for change.[139] With no cohesive national system to address climate change and promote RES growth, states have an unparalleled opportunity to create a multistate forum for cohesive policy change.

C. Harnessing Regional Cooperation to Promote EU Policies

Where the U.S. struggles to create a national framework to develop and support RES growth, the EU faces regional and subnational cooperation challenges in developing the infrastructure needed to achieve its energy transition goals. The EU’s 2018 Ten-Year Network Development Plan (“Development Plan”) identifies the critical need for interconnection and that cooperation between member states remains a key blockage to success.[140] Even under the Development Plan’s fifteen percent interconnection target reformulation, all scenarios analyzed show urgent need for interconnection development in Finland, Greece, Italy, Ireland, Great Britain, and Spain.[141] The Development Plan further reveals that interconnection between member states likely underpins the EU Internal Energy Market (“IEM”) and the EU energy transition’s entire success. The Development Plan concludes that failure to develop the EU grid beyond 2020 could lead to 600 percent regional market price splits at the borders between member states.[142] Further, insufficient interconnection will waste tremendous amounts of renewable energy due to a lack of cross-border capacity for export.[143] This in turn would increase GHG emissions as member states increase local peaking unit production and disincentivize RES growth because new projects would be unable to sell their generation.[144] Therefore, member states must concentrate their efforts on enabling regional interconnection projects at these main blockages.

In order to facilitate critical interconnection projects, the EU must focus on fostering regional and local planning cooperation. Both the Agency for the Cooperation of Energy Regulators and the Development Plan highlight that most PCIs are not yet under construction and cannot guarantee commissioning by 2027.[145] The Development Plan reinforces the Agency for the Cooperation of Energy Regulators’ findings that local acceptability and permitting remains a key obstacle to PCI completion.[146] The Development Plan further suggests that these delays result in expensive redesigns that either delays, reschedules, or requires additional investment in PCIs.[147] Where the Development Plan states that local acceptability “should become a central part of project designs,” its findings indicate that local permitting considerations must be at the heart of project designs.[148] At key blockages, member states must work with local authorities and project managers in commissioning these critical interconnection projects.

VII. RES Policies and National Energy Transitions

Both the EU and U.S. require policy changes to effectuate their current RES and enable future RES advances. However, the revised RED, IEM, and Renewable Portfolio Standards do not operate in a vacuum. The EU and U.S. energy markets necessarily have a tremendous influence on RES growth and energy policy. Understanding past and current policy alone does not result in effective policy change. Instead, the revised RED, IEM, and Renewable Portfolio Standards must be understood in the context of their broader energy markets and the energy transition these markets are favoring. Interestingly, the EU and U.S. energy markets show remarkable similarities in projected future capacity additions and their market drivers. For both the EU and U.S. energy portfolios, natural gas will play a critical in balancing variable RES sources—predominantly wind and solar PV. Further, as both the EU and U.S. transition to greater RES generation, natural gas prices will signal and affect new RES competitiveness.

A. Natural Gas Is Driving Both EU and U.S. Energy Markets

Natural gas will play a crucial role in both the EU and U.S. energy portfolios for the foreseeable future. The EU projects natural gas to comprise around twenty percent of its generation capacity from 2020 through 2050.[149] The U.S. projects natural gas to comprise around thirty-five to forty percent of its generation capacity from 2020 through 2050.[150] Low prices, lower GHG emissions, and increasing efficiency and flexibility to supplement the variable nature of RES all work to make natural gas the preferred replacement for other generation sources such as coal and nuclear.[151]

Both EU and U.S. projections place natural gas in a key but limited role while RES capacity grows, but these projections are based on assumptions that could be significantly affected by natural gas price changes. Low short-term natural gas prices reduce GHG emissions by forcing out coal generation, but prolonged low-priced natural gas may inhibit RES growth and decrease RES competitiveness. In both the EU and the U.S., low natural gas prices may inhibit RES growth over the long term. One study from the University of Texas analyzes natural gas price effects on RES growth in the major U.S. energy markets.[152] The study finds that low natural gas prices below $4.45/MMBtu through 2031 causes RES capacity additions to be reduced by two to three times compared to if natural gas was moderately priced at around $6.67/MMBtu.[153] Low natural gas prices inhibiting RES growth naturally becomes more pronounced the more natural gas dominates a market.[154] Prolonged, low natural gas prices inhibiting RES growth can also be inferred from LACE-LCOE comparisons. Both the EU and U.S. LCOE and LACE-LCOE comparisons assume low natural gas prices through 2030 and beyond to make their calculations.[155] Based in part on low natural gas prices, both the EU and the U.S. project natural gas to be as or more competitive than onshore wind and solar PV.[156] As discussed above, LCOE alone does not capture other significant factors that go into the decision to choose a given generating technology.[157] Critically for the EU, RES growth and LCOE projections are based on meeting the Development Plan interconnection targets that may not be achieved nor adequately address congestion.[158] Should interconnection additions be inadequate, natural gas competitiveness in the EU will impliedly increase as new RES generation cannot be effectively traded across borders.

B. EU and U.S. Policies that Decrease Natural Gas Competitiveness Enable RES Growth

The evidence suggests that decreasing the competitiveness of natural gas catalyzes RES growth. While this finding may seem simplistic on its face, this statement’s power comes from what it does not contain. Because gas prices are a dominant factor in promoting or inhibiting RES growth, certain policy schemes may no longer be effective or require adjustment. In the U.S., gas price effects imply that Renewable Portfolio Standards may no longer be effective for certain states and markets. In the EU, member state NECPs should incorporate gas price scenarios to provide an EU-wide assessment analyzing how member state energy mixes will respond to changing prices and potential interconnection congestion. These implications suggest that the coming battle in the EU and U.S. to increase RES capacity will be one waged not over eliminating coal, but reducing reliance on natural gas.

Natural gas price effects in the U.S. suggest Renewable Portfolio Standards may no longer be effective in many states and markets. Low natural gas prices are pushing out other fossil fuel generation and can “override the effects of RPS.”[159] Both the University of Texas study and Lawrence Berkeley National Lab Renewable Portfolio Standards policies review argue that current and future Renewable Portfolio Standards policy effectiveness will depend on the region and aggressiveness of their targets. Renewable Portfolio Standards policies are projected to be most effective in markets and states where coal generation still occupies a dominant role in the energy mix—predominantly the Midcontinent Independent System Operator[160] and the top coal generating states.[161] Outside Midcontinent Independent System Operator and large coal generating states, Renewable Portfolio Standards have muted effects on both generation additions and GHG emission reductions under current Renewable Portfolio Standards.[162] Only when states pursue aggressive Renewable Portfolio Standards, requiring over fifty percent renewables by 2031, do future generation portfolios significantly change.[163] Therefore, policymakers wishing to promote RES growth through Renewable Portfolio Standards must set far more aggressive targets in the short-term to realize RES gains that would not otherwise be had in a low natural gas price environment.

Natural gas’s role in the developing IEM suggests that EU member states should be developing plans that account for how they will use natural gas in the short-term while looking for ways to reduce their reliance on it in the future. While total EU natural gas use is expected to make up around twenty percent of generating capacity, that percentage varies wildly among individual member states.[164] Some member states project natural gas will occupy only a limited portion of their generating mix, while others project it will be their dominant source of generating capacity.[165] Because the IEM and NECP processes rely on a holistic approach to decarbonization and infrastructure development, risks emerge that countries currently projected to provide the bulk of RES growth could become susceptible to greater reliance on natural gas—especially if interconnection targets are missed at key junctures. The member states that do not expect large amounts of generating capacity to come from natural gas are precisely the ones that need to plan for contingencies if that reality changes. Without an analysis showing how failed interconnection targets and RES curtailment would affect each member state, along with solutions to prevent those effects, market forces and few to no identified alternatives will result in greater natural gas adoption among members states relying on their neighbor’s RES growth. Therefore, member states must take the opportunity in the NECP process to address these risks and identify viable solutions.

Climate change presents the greatest existential crisis of the twenty-first century. Nations around the world must balance the need for development with its effects on their citizens and the world. However, even with current and planned policies, the world will miss the emissions reduction targets needed for the best chance at limiting warming beyond 2℃. Without immediate, aggressive action by developed and developing nations alike, fundamental changes to ecosystems around the world, devastating species loss, and millions of people subjugated to poverty risks from lack of food, water, and other necessities seem assured. With many avenues to reduce GHG emissions and limit warming, energy generation stands as the single leading cause of and opportunity to reduce GHG emissions. To understand what leading nations are doing to reduce energy related emissions and opportunities to improve them, this Article has explored current energy policy frameworks within the EU and the U.S. This analysis revealed key opportunities and critical changes needed in the existing policy frameworks in both the EU and the U.S.

The EU has set ambitious targets for RES growth and energy related GHG emissions reductions. The revised RED and NECP processes hold tremendous opportunity for EU member states to come together and develop the IEM that has eluded the EU for years. However, the top-down approach to the EU’s energy transition reveals that its success will depend on member states and their ability to cooperate and complete interconnection projects that already show signs of tension and delay. By taking an EU wide approach to the energy transition, member states are relying on their neighbors to meet RES and interconnection targets to ease their own growth. If member states are unable to meet those targets and alleviate congestion at key interconnection points throughout the EU, the IEM and broader energy transition will at best become muted. Failure will lead to stranded RES generation that in turn disincentivizes further RES growth and increases reliance on natural gas. Prolonged low-price natural gas and the potential for increased reliance on it by member states highlights a key risk that the NECP process must address. In addition to fostering regional cooperation, identifying key investment needs, and encouraging a just energy transition, the NECP process must also identify solutions to prevent member states from locking in to natural gas if broader EU goals fail to materialize. The reality emerges that the next great challenge in promoting RES growth will come not from reducing coal, but from decreasing the reliance on low-cost natural gas.

As the historic leader and still one of the largest emitters of GHGs, the U.S. has failed to create a national policy framework to address climate change and facilitate RES growth. In the vacuum of national policy, individual states have come together to deliver an energy transition in the U.S. The coalition of states making up the U.S. Climate Alliance presents a tremendous opportunity to grow state cooperation and potentially develop the foundation for a future national policy framework. The NECP process from the EU could inform state action and provide multiple examples and tools to increase state cooperation. While states can approach climate and energy policy from the ground up, many should revisit the tool they historically used to foster RES growth. Renewable Portfolio Standards have been the means to force out coal and increase RES competitiveness among U.S. states. However, the enormous amount of natural gas production and its low cost in the U.S. has made existing Renewable Portfolio Standards irrelevant in many states. Further, projected low-price natural gas now threatens to inhibit RES long-term growth in the U.S. For many U.S. states, aggressive Renewable Portfolio Standard targets in the range of fifty percent RES by 2030 will be required to promote RES growth beyond those signaled predominantly by low natural gas prices. However, many coal generating reliant states would benefit greatly from low to moderate Renewable Portfolio Standard targets. For both the EU and U.S., the projections suggest that their energy futures are ones comprised predominantly by natural gas, wind, and solar PV. These results reveal that natural gas has fundamentally altered the EU and U.S. energy landscapes by outcompeting coal and nuclear. The discussions around broader energy transitions and reducing energy related GHG emissions within the EU and U.S. must now shift to a focus on increasing regional cooperation while reducing reliance on natural gas.

Capacity-weighted and unweighted value-cost ratios for generating technologies entering service in 2023.[166]

- * Peter Mather is currently in government practice. He holds an LLM in International Energy Law and Policy from the University of Dundee’s Centre for Energy, Petroleum and Mineral Law and Policy and a J.D. from the University of Arizona. Thank you to my friends, family, and incredible wife for their love, support, and patience. Thank you to the staff of the Colorado Natural Resources, Energy, & Environmental Law Review for their superb editorial work and thoughtful contributions. ↑

- See U.N. IPCC, IPCC Special Report on Climate Change, Desertification, Land Degradation, Sustainable Land Management, Food Security, and Greenhouse gas fluxes in Terrestrial Ecosystems: Summary for Policymakers (Aug. 7, 2019), https://www.ipcc.ch /srccl/ [hereinafter IPCC Special Report]. ↑

- See UNEP, Emissions Gap Report 2018 (Nov. 27, 2018), https://wedocs.unep.org /bitstream/handle/20.500.11822/26895/EGR2018_FullReport_EN.pdf?sequence=1&isAllowed=y [hereinafter Emissions Gap Report 2018]. ↑

- See U.S. Glob. Change Res. Program, Climate Science Special Report: Fourth National Climate Assessment, Volume I: Our Globally Changing Climate (2017), https://science2017.globalchange.gov/chapter/1/. ↑

- Global Energy & CO2 Status Report: The latest trends in energy and emissions in 2018, IEA, https://www.iea.org/geco/ (last visited Sept. 9, 2019). ↑

- Sustainable Development Scenario: A cleaner and more inclusive energy future, IEA, https://www.iea.org/weo/weomodel/sds/ (last visited Sept. 9, 2019). ↑

- Compare Tracking Clean Energy Progress: Assessing the latest information on how 45 critical energy technologies and sectors are contributing to global clean energy transitions, IEA, https://www.iea.org/tcep/ (last visited Sept. 16, 2018) [hereinafter Tracking Clean Energy Progress], with Emissions Gap Report 2018, supra note 2, at 5 (IEA estimated 32.5 GtCO2 emissions from energy related activities and UNEP estimated 49.2 GtCO2 total global emissions). ↑

- U.N. IPCC, Global Warming of 1.5 ºC: Summary for Policy Makers, at 5 (Oct. 2018), https://www.ipcc.ch/sr15/chapter/spm/ [hereinafter Global Warming of 1.5 ºC]. ↑

- Emissions Gap Report 2018, supra note 2, at xiv. ↑

- IPCC Special Report, supra note 1, at 15. ↑

- Id. at 15. ↑

- Id. at 16. ↑

- Id. ↑

- Id. at 16–17. ↑

- Global Warming of 1.5 ºC, supra note 7, at 7. ↑

- See id. ↑

- Id. at 7–8. ↑

- Id. at 8. ↑

- Id. ↑

- Id. ↑

- Id. ↑

- Id. at 8–9. ↑

- Id. at 9. ↑

- Emissions Gap Report 2018, supra note 2, at 16. ↑

- Paris Agreement to the United Nations Framework Convention on Climate Change art. 4(2), Dec. 12, 2015, T.I.A.S No. 6-1104 [hereinafter Paris Agreement]. ↑

- Emissions Gap Report 2018, supra note 2, at 19. ↑

- Id. at 15. ↑

- Id. at 19. ↑

- See Peter Christoff, The Promissory Note: COP 21 and the Paris Climate Agreement, 25 Envtl. Pol. 765, 766 (2016); Raymond Clemencon, The Two Sides of the Paris Climate Agreement: Dismal Failure or Historic Breakthrough?, 25 J. Env’t & Dev. 3, 9 (2016). ↑

- Paris Agreement, supra note 24, at art. 4(3). ↑

- Emissions Gap Report 2018, supra note 2, at 9. ↑

- Id. at 10. ↑

- Id. Based on interpreting Figure 2.4a as China emitting 15 GtCO2/yr, US emitting 5 GtCO2/yr, India emitting 5 GtCO2/yr, and the EU28 emitting 4 GtCO2/yr. ↑

- Emissions Gap Report 2018, supra note 2, at 9. ↑

- Clemencon, supra note 28, at 3–4. ↑

- Id. at 4, 6. ↑

- Tracking Clean Energy Progress, supra note 6; Emissions Gap Report 2018, supra note 2, at 5 (IEA estimated 32.5 GtCO2 emissions from energy related activities and UNEP estimated 49.2 GtCO2 total global emissions). ↑

- Eurostat, Greenhouse gas emission statistics – emission inventories 3 (2020), https://ec.europa.eu/eurostat/statistics-explained/pdfscache/1180.pdf; EPA, Sources of Greenhouse Gas Emissions, https://www.epa.gov/ghgemissions/sources-greenhouse-gas-emissions (last visited Sept. 9, 2019) (The EPA breaks apart fuel combustion and fugitive emissions between electricity and industry. Within the industry category, emissions from electricity generation are classified as “indirect emissions” and account for roughly 1/3 of total industrial emissions). ↑

- Coal Fired Power, IEA, https://www.iea.org/reports/coal-fired-power (last visited Apr. 13, 2021); Tracking Clean Energy Progress, supra note 6. ↑

- Sources of Greenhouse Gas Emissions, supra note 37. ↑

- 2009 O.J. (L 140) 28. ↑

- Id. at 46. ↑

- Id. at 41–42. ↑

- Id. at 29. ↑

- Infringement Procedure, Eur. Comm’n, https://ec.europa.eu/info/law/law-making-process/applying-eu-law/infringement-procedure_en. ↑

- Council Directive 2018/2001, of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources (recast), 2018 O.J. (L 328) 82, 140 [hereinafter Directive (EU) 2018/2001]. ↑

- Commission Regulation (EU) 2018/1999 of the European Parliament and of the Council of 11 December 2018, Annex I, 2018 (L 328) 1. ↑

- Id. at 14. ↑

- Id. at 16. ↑

- Id. ↑

- Id. at 21. ↑

- Id. at 37. ↑

- Id. at 34. ↑

- Id. at 19. ↑

- Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: Progress towards completing the Internal Energy Market, at 2, COM (2014) 634 final (Oct. 13, 2014), https://ec.europa.eu/energy/ sites/ener/files/documents/2014_iem_communication _0.pdf [hereinafter IEM Progress Report]. ↑

- Id. ↑

- Id. at 7. ↑

- See id. at 8. ↑

- Id. ↑

- Id. ↑

- Comm’n Expert Grp. on Elec. Interconnection Targets, Towards a sustainable and integrated Europe, EU 25 (2017), https://ec.europa.eu/energy/sites/ener/files/documents /report_of_the_commission_expert_group_on_electricity_interconnection_targets.pdf [hereinafter Comm’n Expert Grp.]. ↑

- Agency for the Cooperation of Energy Regulators, Consolidated Report on the Progress of Electricity and Gas Projects of Common Interest for the Year 2017, at 12 (Nov. 7, 2018), https://www.acer.europa.eu/Official_documents/Acts_of_the_Agency/Publica tion/Consolidated%20Report%20on%20the%20progress%20of%20electricity%20and%20gas%20projects%20of%20Common%20Interest%20for%20the%20year%202017.pdf [hereinafter ACER]. ↑

- Id. at 14. ↑

- Id. at 25–32. ↑

- Id. at 31. ↑

- Id. at 18. ↑

- Id. at 17. ↑

- Comm’n Expert Grp., supra note 60, at 25. ↑

- Id. at 24. ↑

- Id. at 25. ↑

- IEM Progress Report, supra note 54, at 15. ↑

- Id. at 13. ↑

- Id. ↑

- Evaluation Report covering the Evaluation of the EU’s regulatory framework for electricity market design and consumer protection in the fields of electricity and gas; Evaluation of the EU rules on measures to safeguard security of electricity supply and infrastructure investment (Directive 2005/89), at 6, SWD (2016) 412 final (Nov. 30, 2016), https://eur-lex.europa.eu/resource.html?uri=cellar:20674470-b7b9-11e6-9e3c-01aa75ed71a1.0001.02/DOC_1&format=PDF. ↑

- Id. ↑

- Id. ↑

- Id. ↑

- Id. ↑

- Id. at 29. ↑

- Id. ↑

- Id. ↑

- Id. at 30. ↑

- Kirsten Engel, Mitigating Global Climate Change in the United States: A Regional Approach, 14 NYU Envtl. L.J. 54, 56 (2005). ↑

- Id. ↑

- Mark Cooper, Governing the Global Climate Commons: The Political Economy of State and Local Action, After the U.S. Flip-flop on the Paris Agreement, 118 Energy Pol’y 440, 445 (2018). ↑

- About Us, U.S. Climate All., https://www.usclimatealliance.org/about-us (last visited Sept. 9, 2019). ↑

- States United for Climate Action, U.S. Climate All., https://www.usclimate alliance.org/ (last visited Sept. 9, 2019). ↑

- EIA, Energy related Carbon Dioxide Emissions by State, 2005-2016: Table 4. 2016 state energy related carbon dioxide emissions by sector (Feb. 2019), https://www.eia.gov/environment/emissions/state/analysis/pdf/table4.pdf [hereinafter Table 4]. ↑

- Engel, supra note 82, at 58. ↑

- Table 4, supra note 87. ↑

- Table 4, supra note 87; About Us, supra note 85. ↑

- Table 4, supra note 87; About Us, supra note 85. ↑

- Emissions Gap Report 2018, supra note 2, at 19. ↑

- What is U.S. electricity generation by energy source?, EIA, https://www.eia. gov/tools/faqs/faq.php?id=427&t=3 (last visited Sept. 10, 2019). ↑

- Id. ↑

- Id. (The remaining 2% from rounding and other sources). ↑

- Almost all power plants that retired in the past decade were powered by fossil fuels, EIA (Jan. 9, 2018), https://www.eia.gov/todayinenergy/detail.php?id= 34452; Nearly half of utility-scale capacity installed in 2017 came from renewables, EIA (Jan. 10, 2018), https://www.eia.gov/todayinenergy/detail. php?id=34472. ↑

- New electric generating capacity in 2019 will come from renewables and natural gas, EIA (Jan. 10, 2019), https://www.eia.gov/todayinenergy/detail. php?id=37952; EIA uses two simplified metrics to show future power plants’ relative economics, EIA (Mar. 29, 2018), https://www.eia.gov/todayinenergy/detail.php?i d= 35552. ↑

- State Renewable Portfolio Standards and Goals, Nat’l Conf. of State Legislatures, http://www.ncsl.org/research/energy/renewable-portfolio-standards.aspx (last visited Sept. 10, 2019). ↑

- Id. ↑

- Galen Barbose, Lawrence Berkeley Nat’l Lab., U.S. Renewable Portfolio Standards: 2018 Annual Status Report (Nov. 2018), http://eta-publications .lbl.gov/sites/default/files/2018_annual_rps_summary_report.pdf. ↑

- Id. at 3, 7. ↑

- Id. at 16. ↑

- Id. at 9. ↑

- Id. at 25. ↑

- Id.; Renewable Energy Certificates (RECs), EPA, https://www.epa.gov/green power/renewable-energy-certificates-recs (last updated May 13, 2019) (RECs are “market-based instrument[s] that represent[] property rights to the environmental, social and other non-power attributes of renewable electricity generation. RECs are issued when one megawatt-hour (MWh) of electricity is generated and delivered to the electricity grid from a renewable energy resource.”). ↑

- Barbose, supra note 100, at 23; EIA, Annual Energy Outlook 2019 with Projections to 2050, at 50 (Jan. 24, 2019), https://www.eia.gov/outlooks/aeo/pdf/aeo 2019.pdf. ↑

- Manussawee Sukunta, EIA Uses Two Simplified Metrics to Show Future Power Plants’ Relative Economics, EIA: Today in Energy (Mar. 29, 2018), https:// www.eia.gov/todayinenergy/detail.php?id=35552. ↑

- Jeffery Logan et al., Nat’l Renewable Energy Lab., Electricity Generation Baseline Report 22 (2017), https://www.nrel.gov/docs/fy17osti/67645.pdf; EIA, Levelized Cost and Levelized Avoided Cost of New Generation Resources in the Annual Energy Outlook 2019 1 (Feb. 2019), https://www.eia.gov/outlooks/archive /aeo19/pdf/electricity_generation.pdf. ↑

- Logan et al., supra note 108, at 22. ↑

- Id. at 23. ↑

- EIA, Levelized Cost and Levelized Avoided Cost of New Generation Resources in the Annual Energy Outlook 2019, at 3 (Feb. 2019), https://www.eia .gov/outlooks/archive/aeo19/pdf/electricity_generation.pdf. ↑

- Id. at 4. ↑

- Id.; Logan et al., supra note 108, at 26. ↑

- EIA, supra note 111, at 11–12. ↑

- For a complete discussion of the EIA’s methodology in arriving at its LCOE, LACE, and cost-value figures see id. at 5–12. ↑

- Id. at 12–13. ↑

- Id. at 12. ↑

- Id. at 13. ↑

- Id. ↑

- Id. ↑

- Id. at 12. ↑

- Id. ↑

- Suparna Ray, New Electric Generating Capacity in 2020 Will Come Primarily From Wind and Solar, EIA: Today in Energy (Jan. 14, 2020), https://www.eia.gov/todayinenergy/detail.php?id=42495. ↑

- See Communication From The Commission To The European Parliament, The Council, The European Economic And Social Committee And The Committee Of The Regions: United in delivering the Energy Union and Climate Action – Setting the foundations for a successful clean energy transition, COM (2019) 285 final (June 18, 2019), https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52019DC0285 &qid=1614097541895 [hereinafter United in Delivering the Energy Union and Climate Action]. ↑

- Id. at 16–20. ↑

- Id. at 16. ↑

- Id. at 17. ↑

- Id. at 18. ↑

- Id. at 19. ↑

- Id. at 20; The Commission defines energy poverty as a situation where a household “needs to spend more than 10% of its income on fuel to maintain an adequate level of warmth.” Energy Poverty, Eur. Comm’n, https://ec.europa.eu/energy/en/eu-buildings-factsheets-topics-tree/energy-poverty (last visited Sept. 10, 2019). ↑

- United in Delivering the Energy Union and Climate Action, supra note 124, at 20. ↑

- Id. ↑

- Id. at 20–21. ↑

- Id. at 21. ↑

- State Policies, U.S. Climate All., https://www.usclimatealliance.org/ state-climate-energy-policies (last visited Sept. 10, 2019); Annual Report, U.S. Climate All., https://www.usclimatealliance.org/annual-report (last visited Sept. 10, 2019); 2018 Strategy, U.S. Climate All., https://www.usclimatealliance.org/2018-strategy (last visited Sept. 10, 2019); Publications, U.S. Climate All., https://www.usclimatealliance.org/publications-1 (last visited Sept. 10, 2019). ↑

- Directive (EU) 2018/2001, supra note 45, at 105. ↑

- See State Policies, supra note 135. For example, Wisconsin’s governor issued an executive order directing the state to transition to 100% RES by 2050 while Colorado has passed legislation and begun strategizing on how to achieve 100% RES by 2040. Wisconsin will undoubtedly begin to look both within and beyond its borders in meeting its RES goals. Colorado and other U.S. Climate Alliance member states assuredly have knowledge and offer opportunities for Wisconsin in reaching its goals. Wisc. Exec. Order No. 2019-38 (Aug. 16, 2019), https://content.govdelivery.com/attachments/WIGOV/ 2019/08/16/file_attach ments/1268023/EO%20038%20Clean%20Energy.pdf; Jared Polis, Polis Administration’s: Roadmap to 100% Renewable Energy by 2040 and Bold Climate Action (2019), https://drive.google.com/file/d/0B7w3bkFgg92dMkpx Y3VsNk5nVGZGOHJGRUV5VnJwQ1U4VWtF/view. ↑

- United in Delivering the Energy Union and Climate Action, supra note 124. ↑

- Eur. Network of Transmission Sys. Operators for Electricity (ENTO-E), TYNDP 2018 Executive Report Connecting Europe: Electricity 2025 – 2030 – 2040 24–29 (2018), https://tyndp.entsoe.eu/Documents/TYNDP%20documents/TYNDP2018/ consultation/Main%20Report/TYNDP2018_Executive%20Report.pdf [hereinafter ENTSO-E]. ↑

- Id. at 35. ↑

- Id. at 36–37. ↑

- Id. at 36, 39. ↑

- Id. at 38–39 ↑

- ACER, supra note 61, at 14; ENTSO-E, supra note 139, at 45–46. ↑

- ENTSO-E, supra note 139, at 46. ↑

- Id. ↑

- Id. at 47. ↑

- Directorate-General for Energy, Directorate-General for Climate Action & Directorate-General for Mobility & Transp., EU Reference Scenario 2016: Energy, Transport and GHG Emissions Trends to 2050, at 64, 70 (2016), https://op.europa.eu/s/oHAX [hereinafter EU Reference Scenario 2016]; Int’l Renewable Energy Agency [IRENA] & Eur. Comm’n, Renewable Energy Prospects for the European Union, at 55 (Feb. 2018), https://www.irena.org/-/media/Files/IRENA/Agency/Publication /2018/Feb/IRENA_REmap_EU_2018.pdf. ↑

- EIA, Annual Energy Outlook 2019, at 21 (2019) [hereinafter Annual Energy Outlook 2019]. ↑

- Id. at 22; EU Reference Scenario 2016, supra note 148, at 66.; How Much Carbon Dioxide is Produced When Different Fuels are Burned?, EIA, https://www.eia.gov/tools/faqs/faq.php?id=73&t=11 (last reviewed June 17, 2020). ↑

- David E. Adelman & David B. Spence, U.S. Climate Policy and the Regional Economics of Electricity Generation, 120 Energy Pol’y 268 (2018). ↑

- Id. at 271. ↑

- Id. at 273. ↑

- Annual Energy Outlook 2019, supra note 149, at 33; EU Reference Scenario 2016, supra note 148, at 37–38. ↑

- Annual Energy Outlook 2019, supra note 149, at 24; EU Reference Scenario 2016, supra note 148, at 42. ↑

- Logan et al., supra note 108, at 22; Levelized Cost and Levelized Avoided Cost of New Generation Resources in the Annual Energy Outlook 2019, EIA (Feb. 2019), https://www.eia.gov/outlooks/aeo/pdf/electricity_generation.pdf; EIA, supra note 106. ↑

- EU Reference Scenario 2016, supra note 148, at 32. ↑

- Adelman & Spence, supra note 151, at 272. ↑

- See MISO, https://www.misoenergy.org (last visited Jan. 24, 2021). MISO includes North Dakota, Minnesota, Iowa, Wisconsin, Michigan, and portions of Montana, South Dakota, Illinois, Indiana, Missouri, Kentucky, Arkansas, Louisiana, Alabama, and Texas. ↑

- See id.; Barbose, supra note 100, at 14 (the Lawrence Berkeley National Lab report captures data from states with RPS policies, not entire market information. The inference that RPS will be most effective in markets and states with a coal dominated energy mix can be drawn in part from the lack of RPS policies in those states). Compare Barbose, supra note 100, at 6, with Energy Consumption Estimates by Source, Ranked by State, EIA (2018), https://www.eia.gov/state/seds/sep_sum/html/pdf/rank_use_ source.pdf. ↑

- Adelman & Spence, supra note 151, at 272; Barbose, supra note 100, at 14. ↑

- Adelman & Spence, supra note 151, at 272. ↑

- Int’l Renewable Energy Agency & Eur. Comm’n, Renewable Energy Prospects for the European Union 56 (2018), https://www.irena.org/-/media/Fil es/IRENA/Agency/Publication/2018/Feb/IRENA_REmap_EU_2018.pdf. ↑

- Id. ↑

- EIA, supra note 111, at 12–13. ↑